Navigating the 2026 Fiscal and Data Frontier

The Great Recalibration: Structural Shifts in UK Property Taxation

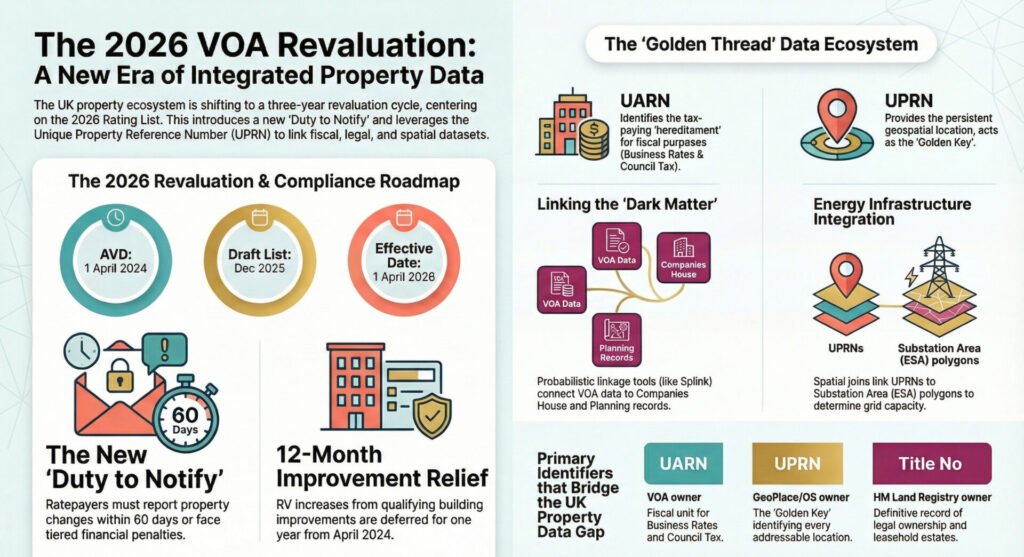

The administration of Non-Domestic Rating in the United Kingdom is currently undergoing its most profound structural transformation since the late 20th century. This shift, codified under the Non-Domestic Rating Act 2023, represents far more than a routine fiscal update: it is a fundamental reimagining of the UK property data infrastructure. The Valuation Office Agency (VOA) is moving from a quinquennial (five-year) revaluation cycle to a triennial (three-year) cycle, a transition designed to ensure that rateable values (RVs) are more sensitive to the volatile economic conditions of the post-pandemic era. By compressing the revaluation timeline, the government aims to reduce the lag between market shifts and tax liabilities, but this agility creates a formidable “data imperative” for all stakeholders (VOA, 2024). The 2026 Revaluation will serve as the first major test of this accelerated system, using an Antecedent Valuation Date (AVD) of 1 April 2024 as its economic baseline. This date crystallises all economic factors, such as prevailing rents and yields, providing a fixed market snapshot for over 2.1 million commercial properties across England and Wales (VOA, 2024).

This transition necessitates a more sophisticated approach to institutional data strategy. The compression of the cycle leaves little room for the historic latency that allowed errors in property descriptions or floor areas to persist across multiple lists. For institutional owners and occupiers, the AVD of April 2024 is the critical junction where physical property characteristics meet contemporary economic reality. To navigate this frontier, one must understand the rigorous statutory timeline that governs the transition from the current 2023 List to the upcoming 2026 List.

2026 Revaluation Milestones | Key Dates | Description |

Antecedent Valuation Date (AVD) | 1 April 2024 | The market snapshot date for rental evidence and yields. |

Publication of Draft List | 31 December 2025 | Initial disclosure of proposed valuations for ratepayer review. |

Effective Date | 1 April 2026 | Date the 2026 Rating List becomes legally chargeable. |

2023 List Challenge Deadline | 31 March 2026 | Final date to initiate a “Check” for the expiring 2023 list. |

This fiscal shift is underpinned by an ontological transformation. As the VOA integrates more closely with HM Revenue and Customs (HMRC), the identifying markers of British property are being standardised to facilitate a more multidimensional analysis of economic productivity (VOA, 2024). This integration, set to be completed by April 2026, signals a future where property tax data is seamlessly linked with VAT turnover and Corporation Tax records, potentially allowing for a more granular analysis of productivity per square metre.

The Ontology of Space: Hereditaments, Identifiers, and the “Many-to-Many” Paradox

At the heart of the British property tax system lies the “hereditament,” a conceptual unit that often defies physical logic. Defined under Section 64 of the Local Government Finance Act 1988, the hereditament is the atomic unit of rateable occupation (VOA, 2024). It is determined by four legal tenets: actual occupation, exclusive occupation, beneficial occupation, and a degree of permanence. Crucially, the hereditament is a fiscal unit, which frequently differs from the spatial or legal unit. To track these units, the VOA utilises the Unique Address Reference Number (UARN), an 11-digit persistent identifier.

The strategic challenge for property analysts lies in the “Many-to-Many” paradox between fiscal identifiers (UARNs) and geospatial identifiers, specifically the Unique Property Reference Number (UPRN). The UPRN is the digital spine managed by GeoPlace, providing a persistent link for approximately 40 million addressable locations (GeoPlace, 2024). However, the mapping between a UARN and a UPRN is rarely straightforward. A single office skyscraper may host hundreds of hereditaments (UARNs), each representing a separate tenant demise, while the building itself is identified by one UPRN. Conversely, a vast industrial campus or university may comprise dozens of buildings but be treated as a single hereditament (one UARN) if the operations are functionally interdependent (VOA, 2024).

A further complication arises with the “Composite Hereditament,” a property that incorporates both domestic and non-domestic elements (e.g., a public house with a landlord flat). In these instances, the commercial portion appears in the rating list, while the domestic portion is banded for Council Tax. This bifurcation creates significant risks for energy intensity calculations, as a single utility meter often serves both units. If analysts calculate energy use using only the commercial floor area, the resulting intensity figure is artificially inflated (VOA, 2024).

Anatomy of the UARN

- Persistence: Unlike local Billing Authority (BA) Reference Numbers, the UARN remains attached to a hereditament across successive rating lists.

- Granularity: The UARN operates strictly at the level of occupation, identifying specific tenancies rather than whole buildings.

- Data Isolation: The UARN is a proprietary VOA identifier. It is not natively found in Land Registry records.

A critical barrier to market transparency is the VOA refusal to release a bulk UARN-to-UPRN lookup table. The agency has cited Section 44(1)(a) of the Freedom of Information Act and Section 23(1) of the Commissioners for Revenue and Customs Act 2005 (CRCA) to maintain this isolation, arguing that linking taxpayer liability to precise locations could disclose commercially sensitive data (VOA, 2024). This opacity forces institutional investors to rely on expensive, proprietary cross-reference products like AddressBase Premium.

Data Integrity as Liability: The Emergence of the “Duty to Notify” Regime

A defining feature of the 2026 fiscal era is the implementation of the “Duty to Notify,” a regime that weaponises administrative inertia by shifting the legal burden of data accuracy from the state to the ratepayer. Phased in between 2026 and 2029, this requirement demands that ratepayers proactively notify the VOA of changes to property characteristics or tenure within 60 days of the event (VOA, 2024). This represents a move away from the historical reliance on periodic “Forms of Return” toward a model of continuous, verified data streaming.

The implications for internal data management are severe. A lack of synchronisation between lease data and physical floor area measurements (NIA or GIA) now constitutes a direct fiscal threat. Failure to comply with these notification requirements triggers a tiered penalty framework. Crucially, the provision of false information carries a significant, uncapped risk: a £500 fixed penalty plus 3% of the difference in Rateable Value (VOA, 2024). For a high-value asset with an RV of £10 million, a 10% discrepancy in reported data could lead to a £30,000 penalty, transforming a back-office oversight into a material balance sheet liability.

Statutory Penalty Framework | RV Tier | First Offense Penalty | Continuing Non-Compliance (Daily) |

Small | Up to £15,000 | £300 Fixed Penalty | £60 per day |

Medium | £15,001 – £51,000 | £600 Fixed Penalty | £60 per day |

Large | Over £51,000 | £900 Fixed Penalty | £60 per day |

The necessity for precision is further underscored by the government transitional relief mechanisms. For the 2026 List, properties seeing a reduction in RV will receive the full benefit of that reduction immediately (VOA, 2024). Conversely, upward shifts in liability will be capped and phased in. However, if a property is over-valued due to inaccurate floor area data, the ratepayer is effectively denied an immediate cash saving. In this context, data integrity is not merely a compliance burden but a vital tool for liquidity management.

The Valuation Void: Methodological Blind Spots and “Missing” Floor Area

The VOA utilises three primary methodologies to determine value: the Comparative (Rental) method, the Receipts and Expenditure (R&E) method, and the Contractor’s Basis. While the Comparative method (used for shops, offices, and warehouses) generates robust floor area data, the other methods create a “valuation void” that can frustrate energy modelling and asset management (VOA, 2024).

The “Missing Floor Area” trap is particularly prevalent in the R&E method, often used for public houses (SCat 226) and hotels (SCat 131). Because value in these sectors is derived from “Fair Maintainable Trade” and accounts rather than physical dimensions, the VOA frequently does not record or publish floor area statistics for these assets (VOA, 2024). Similarly, the Contractor’s Basis, used for specialised assets like schools and hospitals, is based on replacement cost, leading to these properties being categorised as “Excluded” in standard floorspace statistics. This is a significant blind spot for public sector decarbonisation strategies.

Furthermore, the VOA adherence to the RICS Code of Measuring Practice introduces systemic discrepancies in energy intensity benchmarks. Analysts must distinguish between:

- Net Internal Area (NIA): Utilised for Offices (SCat 203) and Retail units (SCat 249G), this excludes common areas such as toilets, lift lobbies, and plant rooms.

- Gross Internal Area (GIA): Utilised for Industrial units (SCat 096G) and Large Distribution Warehouses (SCat 151S), this includes the entire area inside the external walls.

When calculating energy intensity (kWh/m2), using NIA as a denominator artificially inflates a building’s energy profile because the energy consumption of “free-rider” common parts is being attributed to a smaller usable area. This distinction is critical for identifying the “Performance Gap,” the discrepancy between a building theoretical efficiency (as stated on an EPC) and its actual operational energy use (VOA, 2024). Studies suggest that VOA floor area data is often more reliable than EPC data for this purpose, provided the NIA/GIA mismatch is corrected.

RICS Code of Measuring Practice: Sectoral Mapping

- Offices and Retail (Bulk Class): Measurement by NIA. High risk of undercounting energy-intensive common parts.

- Industrial and Logistics (SCat 096G, 151S): Measurement by GIA. Includes loading bays and internal partitions.

- Specialist Leisure (R&E Method): Frequently lacks published floorspace data. Requires alternative geometric extraction from OS MasterMap.

The Energy Frontier: Power Availability as a Material Valuation Constraint

The 2026 Revaluation arrives at a moment when “power availability” has become a material constraint on property value. For industrial and logistics sectors (SCat 151S), the ability of a property to support electric vehicle (EV) fleets or heat pumps is increasingly dictated by “Network Headroom” (National Grid, 2024). This creates a new form of “locational disability.”

Properties located in “Red” zones (areas with zero demand headroom) face significant capital expenditure requirements to upgrade grid connections. Under VOA valuation principles, such constraints can be argued as grounds for a reduction in Rateable Value, as the lack of infrastructure impairs the rental value of the asset compared to a similar property in a “Green” (high capacity) zone (VOA, 2024). This is particularly relevant for Data Centres (SCat 068S for converted units and SCat 069S for purpose-built units), where power availability is the primary determinant of rent. Capturing these variables requires a spatial join between UPRN coordinates and Electricity Substation Area (ESA) polygons.

Simultaneously, the regulatory environment is shifting to incentivise green investment. Under the Valuation for Rating (Plant and Machinery) (England) (Amendment) Regulations 2022, specific technologies are exempt from business rates until 2035 (HMRC, 2024).

Green Technology Exemptions (2022-2035)

- Renewable Generation: Plant used for solar (SCat 743), wind (SCat 744), and biomass generation is excepted from rating.

- Energy Storage: Battery systems (SCat 733) used for renewables or EV charging points are exempt.

- District Heating: Low-carbon heat networks receive relief to support decarbonisation.

While these exemptions remove fiscal barriers to retrofitting, they also make these assets “invisible” in traditional tax-based datasets. A rooftop solar array may no longer increase a building RV, but its absence from the rating list complicates the task of tracking national renewable capacity (VOA, 2024). Furthermore, the “Improvement Relief” operative from April 2024 allows ratepayers to defer RV increases for 12 months following qualifying works, creating a lag in data visibility.

Illuminating the “Dark Matter”: Probabilistic Linkage and the “Golden Thread”

A vast portion of the property data universe consists of “dark matter,” public datasets that lack the persistent identifiers (UARNs or UPRNs) necessary for easy integration. Records from Companies House, planning appeals, and Food Standards Agency (FSA) hygiene ratings contain immense value for predicting occupancy risk and market shifts, but they often exist as messy, free-text strings (VOA, 2024).

To bridge this gap, the industry has adopted probabilistic record linkage, specifically utilising the “Splink” library developed by the Ministry of Justice. This methodology, based on the Fellegi-Sunter model, allows analysts to “hydrate” dry text data with geospatial intelligence. Instead of simple exact matching, Splink calculates the probability that two records refer to the same property by analysing term frequency (e.g., recognising that a match on “Zebedee Lane” is more significant than a match on “High Street”).

However, the “match rate” for this process varies significantly by sector. Research indicates that “Shops” have a notably low match rate (approximately 38%) due to complex sub-divisions and inconsistent addressing in retail parades. In contrast, “Warehouses” achieve much higher match rates (approximately 74%) because their addressing is typically simpler and more stable (VOA, 2024).

The Probabilistic Linkage Strategy

- Filtering: Isolate relevant records, such as “Live” companies at trading locations, while excluding administrative “brass plate” addresses.

- Matching (Term Frequency): Parse address strings and apply weights based on the rarity of terms to avoid false positives in high-density areas.

- Validation: Cross-reference synthetic UPRNs with the VOA Rating List to ensure the Rateable Value aligns with the business size and type (SIC code).

This technological capability allows for the creation of a “Golden Thread” of information that binds fiscal, legal, physical, and utility data into a single, interoperable view (GeoPlace, 2024). For the 2026 era, this thread is the difference between reactive management and strategic advantage.

Strategic Synthesis: The Maturation of the Digital Property Ecosystem

The 2026 Revaluation will be defined less by the values it sets and more by the digital ecosystem that underpins it. We are entering an era where data integrity is no longer a peripheral administrative concern but a core component of fiscal compliance and asset valuation. The transition to a triennial cycle and the imposition of the Duty to Notify demand a level of data hygiene that many institutional investors are only beginning to implement.

The 2026 List will likely reflect a market where the “flight to quality” in the office sector (SCat 203) is crystallised, and the surge in e-commerce has pushed industrial rents (SCat 151S) to new heights. For the professional and institutional audience, the recommendations are as follows:

- Interoperability is Advantage: The ability to link disparate datasets, such as DNO headroom, HMLR titles, and VOA UARNs, via the UPRN is the primary tool for identifying “locational disabilities” and potential over-valuations.

- Data Integrity is Compliance: The VOA tiered penalty framework, particularly the 3% penalty on RV differences for false information, means that inaccurate records are now a material financial risk. Institutional owners should audit floor area measurements (NIA vs GIA) and link them to lease terms before the 2026 Effective Date.

- Monitor the AVD: All strategic decisions for the 2026 List must be viewed through the lens of the 1 April 2024 market baseline. Any economic shifts after this date are irrelevant for the 2026 valuation, making the snapshot date the absolute authority for rental evidence.

- Mind the Gap: Recognise the “missing floor area” in R&E and Contractor’s Basis properties. Do not assume a zero in floorspace statistics represents a lack of size; rather, it indicates that physical dimension was not the primary basis of valuation (VOA, 2024).

The 2026 Rating List will serve as a stress test for the UK property data infrastructure. Those who can weave the “Golden Thread” between fiscal mandates and spatial reality will find themselves best positioned to navigate the complexities of this new digital property frontier. Data is no longer the substrate of property management: it is the asset itself.

Bibliography

Advanced Infrastructure (2024) Electricity Substation Supply Areas Generation Headroom Dataset. Available at: https://www.advanced-infrastructure.co.uk/datasets/electricity-substation-supply-areas-generation-headroom-dataset (Accessed: 24 May 2024).

Department for Energy Security and Net Zero (DESNZ) (2024) National Energy Efficiency Data-Framework (NEED) Methodology for Non-Domestic properties. London: DESNZ.

GeoPlace LLP (2024) Persistent and well-behaved identifiers. Available at: https://www.geoplace.co.uk/blog/persistent-and-well-behaved-identifiers (Accessed: 24 May 2024).

HM Government (2023) Non-Domestic Rating Act 2023. London: The Stationery Office.

HM Land Registry (2024) Technical specification Title Number and UPRN Look Up dataset. Available at: https://use-land-property-data.service.gov.uk/datasets/nps/tech-spec/2 (Accessed: 24 May 2024).

HMRC (2024) The Valuation for Rating (Plant and Machinery) (England) (Amendment) Regulations 2022. London: HMRC.

Ministry of Justice (MoJ) (2022) Splink: Fast, accurate and scalable record linkage. Available at: https://dataingovernment.blog.gov.uk/2022/09/23/splink-fast-accurate-and-scalable-record-linkage (Accessed: 24 May 2024).

National Grid (2024) Network Headroom Report. Available at: https://commercial.nationalgrid.co.uk/downloads-view-reciteme/398146 (Accessed: 24 May 2024).

Ordnance Survey (2024) AddressBase Premium Documentation. Southampton: Ordnance Survey.

Valuation Office Agency (VOA) (2024) Annual Report and Accounts 2023-24. London: VOA.

Valuation Office Agency (VOA) (2024) Non-domestic rating: Stock of properties including business floorspace Background Information. London: VOA.

Valuation Office Agency (VOA) (2025) SCat Codes and Primary Description Codes: as at 28 August 2025. London: VOA.