An Energy-as-a-Service Framework for Post-Conflict Syria

Executive Summary

This document presents a strategic proposal for utility-led distributed energy storage (DES) in post-conflict Syria, structured as an Energy-as-a-Service (EaaS) framework. It draws on international evidence from pioneering programmes in the United States, Australia, Lebanon, and other markets, extracting both positive models and cautionary lessons to inform a deployment strategy calibrated to Syria’s specific conditions as of early 2026.

Syria’s energy crisis is acute: generation capacity has collapsed from approximately 8,500 MW pre-conflict to roughly 3,500 MW, with actual output far lower due to chronic fuel shortages. Electricity supply remains limited to two to four hours daily across much of the country, and transmission and distribution losses exceed 30%. The fall of the Assad regime in December 2024 and the formation of the transitional government have opened a window for reform, reinforced by the lifting of US sanctions in mid-2025 and the repeal of the Caesar Act in December 2025. However, institutional weakness, financial system disconnection from global banking, and unresolved territorial and political disputes pose severe implementation risks.

The proposal introduces a dedicated Special Purpose Vehicle, the Syria Distributed Energy Company (SDEC), to bypass institutional capacity constraints; a “Corridors of Confidence” geographic targeting model aligned with existing grid rehabilitation investments; a two-track approach combining new utility-owned installations with a Bring Your Own Device (BYOD) integration programme for Syria’s substantial existing solar-plus-storage base; and a sequenced financing architecture that bridges the period between sanctions relief and full financial system normalisation. The programme is positioned not as a standalone initiative but as a complementary layer to the national grid rehabilitation strategy already underway.

1. Introduction: The Concept and International Evidence

1.1 The Problem: Fragmented Energy in Weak-Grid Environments

When centralised electricity grids fail, whether through conflict, chronic underinvestment, or natural disaster, affected populations do not simply go without power. They improvise. Households and businesses procure diesel generators, install rooftop solar panels, purchase batteries, and establish informal neighbourhood distribution arrangements. The result is a fragmented energy landscape characterised by extreme cost inequality, environmental degradation, and a self-reinforcing cycle that undermines the economic case for grid restoration. The wealthier a household’s private backup system, the less willing that household is to pay for grid reconnection; the fewer paying customers the grid serves, the harder it becomes to finance rehabilitation.

This pathology is visible across a wide range of contexts. It defines Lebanon’s decade-long electricity crisis, where private diesel generator operators have built a multi-billion-dollar parallel industry. It is evident in Iraq’s post-conflict reconstruction, in Nigeria’s chronic supply deficit, and in the aftermath of natural disasters from Puerto Rico to the Philippines. It is now Syria’s defining infrastructure challenge.

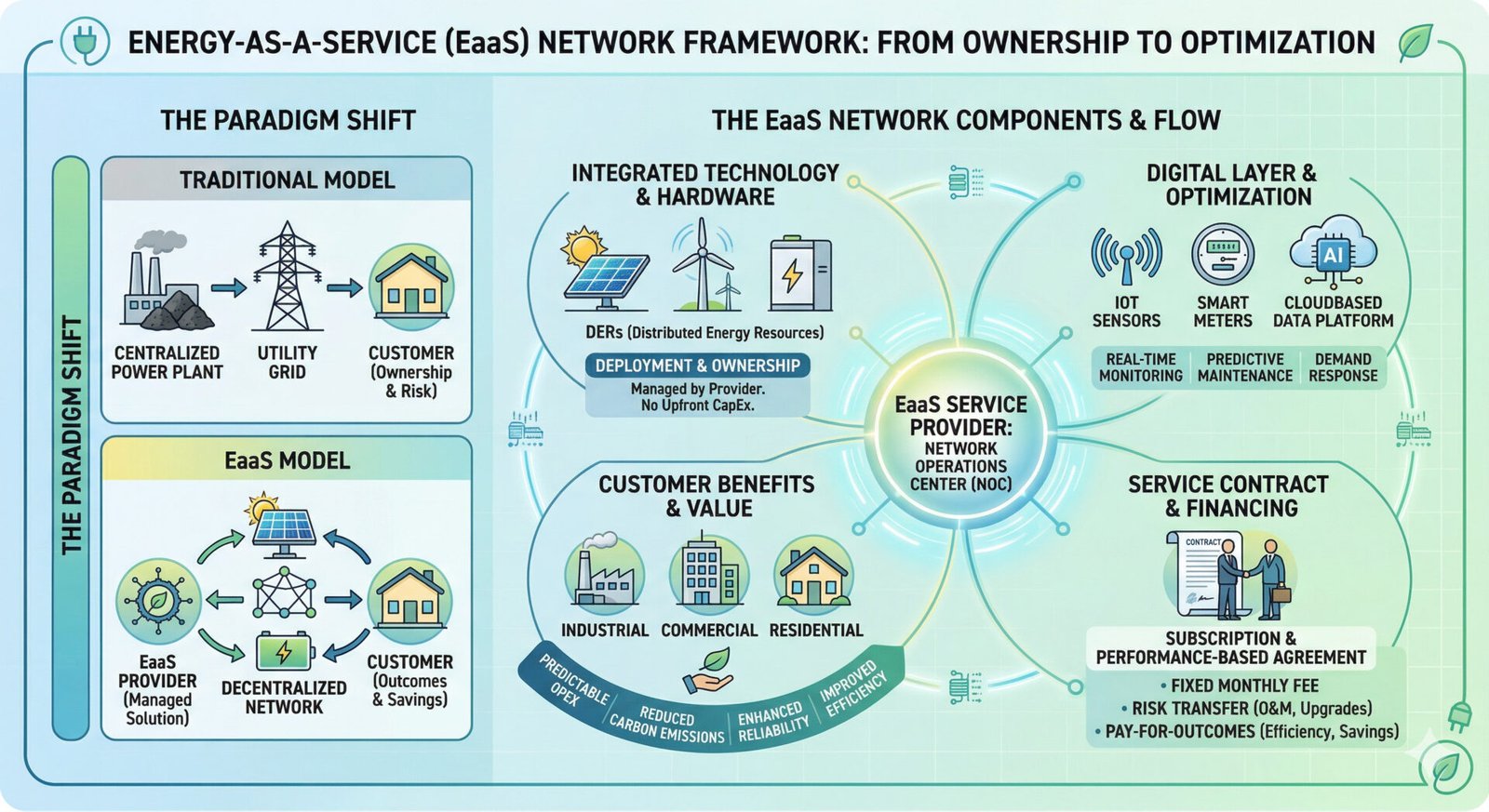

1.2 The Solution: Utility-Led Distributed Energy Storage as a Service

Distributed energy storage (DES), specifically lithium iron phosphate (LiFePO4) battery systems deployed at the household and community level, offers a path out of this trap. The core proposition is straightforward: rather than leaving households to procure their own backup power solutions (which are typically expensive, low-quality, and uncoordinated), the utility deploys professional-grade battery-plus-inverter systems to subscribing households and retains ownership and operational control. The household receives guaranteed backup power and reduced energy costs; the utility gains a fleet of distributed assets that can be aggregated into a Virtual Power Plant (VPP) and dispatched centrally for grid services such as peak shaving, frequency regulation, and load smoothing.

This model is referred to as Energy-as-a-Service (EaaS): the household subscribes to a service (reliable energy) rather than purchasing a product (a battery). The utility absorbs the capital expenditure and recovers costs through a combination of monthly subscription fees and grid-service revenue. The financial logic depends on the fleet being large enough to generate meaningful grid-level value, and on the billing and communications infrastructure being reliable enough to sustain the subscription model.

1.3 Triple-Input Dispatch and Battery Intelligence

At the core of the EaaS model is an intelligent dispatch system governing each battery unit. The system takes three inputs. The first is household demand: the battery monitors real-time household consumption and prioritises covering gaps when grid supply is interrupted. The second is solar generation (where applicable): when paired with rooftop solar, the battery stores excess daytime generation for evening use, maximising self-consumption. The third is utility dispatch signals: the central Distributed Energy Resource Management System (DERMS) can issue charge or discharge instructions to the battery to serve grid-level objectives, such as absorbing excess generation during off-peak periods or injecting stored energy during peak demand.

The critical design principle is that household resilience always takes precedence. A minimum State of Charge (the “Resilience Reserve”) is maintained at all times, ensuring that the utility’s dispatch commands cannot leave the household without backup power. This is not merely a technical feature; it is the political and social foundation of the programme’s legitimacy, particularly in a post-conflict society where trust in state institutions is profoundly eroded.

1.4 International Evidence: Lessons to Build On

Green Mountain Power, Vermont (United States): The Pioneer

Green Mountain Power (GMP), Vermont’s largest electric utility serving approximately 275,000 customers, is the world’s most advanced utility-led residential battery programme and the primary model for this proposal. GMP began offering home battery systems through pilot programmes in 2017, partnering with Tesla as the first utility in the United States to do so. By 2020, it had secured regulatory approval for fully tariffed battery programmes. As of early 2025, GMP has deployed over 8,000 residential batteries across more than 4,500 customers, aggregating approximately 70 MW of stored energy across all asset types, making it the largest power source in Vermont and saving all customers an estimated US$3 million annually in avoided peak demand charges.

GMP operates two complementary tracks. The first is a direct lease programme, in which the utility owns and deploys battery systems (originally Tesla Powerwalls, now also Enphase IQ systems) to subscribing households at approximately US$55 per month or a one-time payment of US$5,500. The utility retains the right to dispatch these batteries during peak demand events. The second is the Bring Your Own Device (BYOD) programme, in which customers who purchase their own battery systems receive rebates of up to US$10,500 in exchange for agreeing to share stored energy during peak events. Demand for both programmes has consistently exceeded available capacity, with waitlists of over 1,000 customers.

GMP’s programme was catalysed by increasingly severe weather events in Vermont, including devastating flooding in 2023 that highlighted the vulnerability of rural distribution infrastructure. The utility has since integrated residential batteries into its broader Resiliency Zones strategy, targeting areas selected using outage statistics and community vulnerability data. In 2025, GMP proposed a US$30 million programme to deploy up to 1,200 batteries free of charge to the most remote homes in southern Vermont, where burying transmission lines is not feasible, with priority given to customers using medical devices and those with lower incomes. A pilot in the town of Grafton achieved a 72% enrolment rate among eligible customers.

Key lessons for Syria: the dual-track model (utility-owned plus BYOD) is essential for engaging existing assets; demand consistently outstrips supply, suggesting that the programme should plan for scaling from the outset; targeting based on vulnerability and outage data is both equitable and politically defensible; and the programme’s primary political appeal is resilience against outages, not abstract grid optimisation.

AEMO Virtual Power Plant Demonstrations (Australia): Proving the Grid Value

The Australian Energy Market Operator (AEMO) ran a landmark VPP demonstration programme from 2019 to 2021, enrolling approximately 7,150 consumers across eight VPP portfolios with a total registered capacity of 31 MW. The programme was motivated by Australia’s world-leading uptake of rooftop solar (over 2.5 million systems exceeding 10 GW of combined capacity) and the need to understand how aggregated distributed resources could participate in wholesale electricity and frequency control ancillary services (FCAS) markets.

The trials demonstrated that coordinated residential batteries could effectively deliver contingency FCAS, responding to frequency excursions within seconds. In a notable event, the South Australian VPP detected a 748 MW generator trip and responded immediately to inject power and aid frequency recovery. VPPs also demonstrated the ability to arbitrage wholesale price signals, pre-charging before anticipated high-price events and discharging during them. However, the programme also revealed important limitations: VPP behaviour proved difficult to forecast, with battery response to price events being smaller and less predictable than AEMO’s models assumed; operational error rates remained higher than acceptable for full FCAS market participation; and approximately 5–8% of fleet data was missing at any given time due to communication issues, even in Australia’s well-developed telecommunications environment.

The financial picture was sobering. Total programme costs exceeded US$7 million, far greater than the combined FCAS revenue earned by all participants. Simply Energy’s VPP earned an estimated US$25 per customer per year in FCAS revenue, insufficient as a standalone business case. The IEEFA concluded that while VPP margins for operators were currently thin, strong growth potential existed as the grid transitioned further toward variable renewable energy.

Key lessons for Syria: VPP grid-services revenue alone cannot sustain the financial model in the early years; the communications infrastructure must be highly reliable for effective dispatch, and Syria’s damaged telecommunications network represents a critical bottleneck; the resilience and backup-power value to the household must carry the financial model initially, with grid-services revenue growing as fleet scale and grid capability mature; and regulatory frameworks for VPP market participation must be developed deliberately, not assumed.

Lebanon: The Cautionary Counter-Model

Lebanon represents the clearest warning of what happens when fragmented energy provision is allowed to consolidate into an entrenched parallel industry without utility intervention. The state utility, Electricité du Liban (EDL), has been unable to provide more than a few hours of electricity per day for over a decade. A network of private diesel generator operators filled the gap, creating a multi-billion-dollar industry estimated at over US$2 billion annually, exceeding EDL’s own revenue. These operators, widely referred to as the “generator mafia,” developed territorial control over neighbourhood-level distribution, established pricing cartels, and cultivated political connections to resist reform.

Attempts to regulate this industry have met fierce resistance: when the town of Zahle successfully collectivised its electricity supply and eliminated generator operator control, providing 24/7 power to its 250,000 residents at lower cost, generator owners burned tyres, blocked roads, and fired shots at electricity infrastructure. The broader picture is one of regulatory capture: Human Rights Watch documented how the failure to activate an independent Electricity Regulatory Authority (mandated by law since 2002, only appointed in September 2025) enabled decades of unchecked exploitation. The poorest 20% of Lebanese households lack generator access entirely, while the poorest quintile that does subscribe spends an estimated 88% of income on electricity.

Lebanon has also seen a rapid but uncoordinated solar adoption, with photovoltaic capacity growing roughly sevenfold between 2020 and 2022. However, this expansion has occurred without grid integration, quality standards, or a mechanism for aggregating distributed assets into a coordinated system. The result is a dual fragmentation: diesel generators serving the majority who can afford them, and private solar serving the wealthy minority, with neither contributing to grid recovery.

Key lessons for Syria: early intervention is essential; once a fragmented energy economy becomes entrenched with vested interests and political protection, reform becomes exponentially harder; any programme must actively prevent the emergence of intermediaries who profit from grid dysfunction; and uncoordinated solar deployment, while better than nothing, does not substitute for a structured EaaS programme that can aggregate distributed assets for grid benefit.

South Australia Tesla VPP: Scale Ambition and Delivery Risk

The South Australian government’s partnership with Tesla to create one of the world’s largest VPPs illustrates both the ambition and the delivery challenges of large-scale residential battery programmes. Originally conceived as a three-phase project targeting 50,000 public housing homes with a combined 250 MW and 650 MWh network of decentralised assets, the project demonstrated successful FCAS market participation at 10 MW capacity. However, scaling from a demonstration to a state-wide deployment proved far more complex than anticipated, with regulatory, logistical, and customer acquisition challenges slowing progress. The gap between announced ambition and operational reality is a recurring pattern in utility-led DES programmes globally.

Key lessons for Syria: phased deployment with conservative scaling assumptions is preferable to ambitious headline targets; public housing and social infrastructure make natural starting points as they avoid the customer acquisition problem; and the gap between a successful pilot and a scaled programme is large and should not be underestimated.

1.5 Synthesis: What the International Evidence Tells Us

Taken together, the international evidence points to several clear principles for a Syria-adapted programme. First, the EaaS model works technically and can deliver real resilience benefits to households. Second, the household-level value proposition (backup power, outage protection) must carry the economic model in early phases; grid-services revenue is real but takes time and scale to materialise. Third, engaging existing distributed assets through a BYOD-type programme is as important as deploying new ones. Fourth, the communications and billing infrastructure is as critical as the battery hardware. Fifth, early regulatory and institutional action is essential to prevent the fragmented energy economy from solidifying into an entrenched, reform-resistant structure. Sixth, scaling is harder than piloting, and conservative deployment timelines protect credibility.

The remainder of this document translates these principles into a strategic framework tailored to Syria’s specific institutional, financial, political, and technical conditions.

2. Strategic Framework

2.1 Strategic Positioning: Complementary Layer, Not Standalone Programme

The distributed EaaS programme should be explicitly positioned as a complementary layer to the national grid rehabilitation strategy, not a parallel or competing initiative. The current reconstruction landscape includes the World Bank Syria Electricity Emergency Project (US$146 million for high-voltage transmission rehabilitation, implemented by PETDE), the SOCAR gas pipeline agreement (1.2 billion cubic metres annually to power plants in Aleppo and Homs), the UCC Holding consortium’s US$7 billion deal for 4 GW of combined-cycle gas turbine plants and 1 GW of solar, and the ACWA Power agreement for 2.5 GW of renewable capacity. These represent the primary investment axis for Syria’s energy recovery: centralised generation capacity restoration and high-voltage transmission rehabilitation.

The distributed EaaS programme addresses a different problem: the “last mile” quality gap between the transmission backbone and the household, particularly in areas where the distribution network is degraded and grid supply is intermittent. This positioning is strategically important because it avoids competition for the same funding streams, offers immediate, visible improvement in household-level service quality while centralised rehabilitation progresses over three to five years, and creates the institutional and technical infrastructure for future VPP aggregation once the distribution grid can support bidirectional flows.

2.2 Revised Institutional Architecture

The Public Establishment for Transmission and Distribution of Electricity (PETDE), the national grid operator, is already stretched as the implementing agency for the World Bank’s SEEP project. The World Bank’s own documentation acknowledges PETDE’s limited institutional capacity, requiring an international consulting firm as Owner Engineer and a third-party monitoring agent. Tasking this same institution with the simultaneous management of thousands of distributed battery endpoints would risk overwhelming an already constrained organisation. The programme should therefore be housed in a dedicated Special Purpose Vehicle.

The Syria Distributed Energy Company (SDEC)

A dedicated SPV, the Syria Distributed Energy Company (SDEC), should be established as a joint venture between the Ministry of Energy (holding a golden share for strategic oversight), a qualified international energy services company as technical and operational partner, and a multilateral development bank-backed financing vehicle providing the capital structure. The SPV model ringfences the programme’s finances and operations from PETDE’s broader institutional challenges; allows international technical partners to bring operational expertise (DERMS management, fleet maintenance, billing systems) without requiring PETDE to develop these capabilities immediately; creates a bankable entity that can attract blended finance on commercial terms; and establishes a regulatory precedent for licensed independent service providers in Syria’s electricity sector, aligning with the institutional reforms being supported under SEEP Component 3.

2.3 Geographic Targeting: The “Corridors of Confidence” Model

Rather than generic targeting based on grid weakness alone, this proposal introduces a geographic strategy aligned with areas of highest institutional stability, returnee population density, and grid connectivity.

Priority Corridor 1: Damascus–Homs Axis

This corridor benefits from the Deir Ali power station (Syria’s largest, receiving Jordanian gas via the Arab Gas Pipeline), proximity to the SEEP substation rehabilitation sites, and relatively stable transitional government control. The high concentration of returnee populations and the political symbolism of improved services in the capital make this the lowest-risk, highest-visibility starting point.

Priority Corridor 2: Aleppo–Hama Industrial Zone

The SOCAR gas pipeline from Turkey is supplying gas to Aleppo’s thermal power plant, generating up to 900 MW. The Hassia Industrial Zone near Homs has already seen 40 MW of solar connected to the national grid. This corridor combines industrial demand (which provides daytime load for solar self-consumption) with residential need, and the existing gas-to-power infrastructure provides a reliable grid backbone.

Priority Corridor 3: Deferred — Northeast Syria

Despite the northeast’s energy resource importance (oil and gas fields), the unresolved political situation with the SDF and ongoing tribal tensions make distributed asset deployment premature. This corridor should be deferred until the fourteen-point integration agreement is substantially implemented and security conditions stabilise.

2.4 Engaging the Existing Distributed Solar Base

Syria’s existing distributed energy landscape is fundamentally different from a greenfield market. Standalone solar PV systems combined with battery storage reached an estimated 1.4 GW of combined capacity by end-2024, driven by grassroots adoption during the conflict. This is not a low-quality generator economy in the Lebanese mould; it is a distributed solar-plus-storage ecosystem that, while uncoordinated, represents a massive installed asset base. Any EaaS strategy must engage with this reality rather than proposing wholesale replacement.

Track A: New Utility-Owned LiFePO4 Installations

This follows the GMP model: the SDEC deploys professional-grade LiFePO4 hybrid systems to critical nodes (health clinics, water infrastructure, apartment clusters) and subscribing households, retaining ownership and operational control. These systems are enrolled in the DERMS platform from day one.

Track B: “Bring Your Own Device” (BYOD) Integration Programme

Drawing directly on GMP’s successful BYOD programme, the SDEC should offer owners of existing solar-plus-storage systems the option to connect to the DERMS platform in exchange for grid service credits. This requires a technical qualification process (only systems meeting minimum safety and communication standards would be eligible), the installation of a smart gateway device enabling DERMS communication, and a compensation structure providing bill credits when the system responds to grid dispatch signals. This track avoids the political and economic costs of asking households to surrender assets they purchased during the conflict for self-reliance. It leverages existing investment rather than writing it off, and rapidly expands the aggregated fleet size without proportional capital expenditure.

2.5 Billing and Compensation Architecture

Billing models must be adapted for Syria’s cash economy and weak banking infrastructure. The financial system remains largely disconnected from global correspondent banking networks, despite the lifting of US sanctions on 1 July 2025 and the repeal of the Caesar Act in December 2025. The Central Bank of Syria has a 2025–2030 reform roadmap, but international banks remain cautious due to residual compliance uncertainty.

Component | Mechanism | Syria Adaptation | Rationale |

Hardware Lease | Fixed monthly availability fee (e.g. US$15–25/month) | Payable via mobile money or prepaid scratch cards | Bypasses broken banking system; leverages mobile penetration |

Grid Service Credit | Bill reduction when battery dispatched for peak shaving | Credit applied to official electricity bill as a line-item discount | Builds trust in utility dispatch; visible economic benefit |

BYOD Incentive | Monthly credit for connected BYOD systems | US$5–10/month credit conditional on 90%+ uptime | Incentivises voluntary integration of existing assets |

Critical Node Subsidy | Zero-cost deployment to health/water infrastructure | Funded by MDB grant component; no end-user charge | Humanitarian rationale; builds public trust in programme |

2.6 The Resilience Reserve: A Non-Negotiable Design Principle

The “trust deficit” in Syria is not merely a consumer psychology challenge; it is a product of thirteen years of state failure. If the utility is perceived as capable of emptying a household’s battery before a blackout, the programme will face active resistance. Drawing on the Lebanese lesson, where distrust of institutional energy provision drove households toward self-reliance at enormous cost, the Resilience Reserve must be the programme’s most visible feature.

The revised framework mandates: a minimum 40% State of Charge (SoC) reserved for household use at all times; a real-time mobile application displaying current SoC, resilience level, and grid dispatch history; a hardware-enforced SoC floor that cannot be overridden by the central DERMS, ensuring that even a compromised or misconfigured central system cannot drain the battery below the reserve; and automatic exclusion from the dispatchable pool for households with registered medical equipment, following GMP’s model of prioritising medical device users.

3. Risk Assessment and Mitigation

3.1 Political Economy Risks

Risk: Capture by Emerging Power Brokers

Syria’s post-conflict environment is characterised by the emergence of new patronage networks. The UCC Holding consortium, a central player in the national energy recovery, is led by individuals currently facing legal proceedings in the United Kingdom. The risk that an EaaS programme is captured by, or becomes dependent upon, actors with contested legitimacy is substantial. Mitigation requires transparent and competitive procurement managed through the SPV with MDB oversight, geographic deployment decisions made on technical criteria (grid weakness, returnee density) rather than political allocation, and independent auditing of the SDEC’s operations by the MDB financing partner.

Risk: Territorial Instability

Distributed assets are physically located in households and communities. If areas where systems are deployed experience renewed conflict or governance changes, the assets may be lost, damaged, or appropriated. The “Corridors of Confidence” targeting strategy mitigates this by concentrating initial deployment in the most stable areas. Political risk insurance from MIGA or similar agencies should be explored.

Risk: Emergence of a “Generator Mafia” Dynamic

Lebanon’s experience demonstrates that without early intervention, informal energy providers can consolidate into politically protected cartels. In Syria, the risk is that operators of existing diesel generators or unregulated solar installers resist the EaaS programme to protect their revenue streams. The BYOD integration track serves as mitigation: by offering existing asset owners a path into the formal system with financial incentives, the programme converts potential opponents into participants.

3.2 Technical Risks

Risk: Distribution Grid Incompatibility

A utility-dispatched VPP requires a functioning distribution grid through which battery energy can flow. In Syria, the distribution network is severely degraded: pre-conflict transmission losses were already 26%, and the conflict has worsened this considerably. Deploying professional-grade LiFePO4 systems to households connected to a distribution grid that cannot reliably deliver or accept power creates stranded assets. Mitigation requires a mandatory distribution grid assessment before deployment in any feeder area. If distribution-level investment exceeding a defined cost per household is required to enable bidirectional flow, the area should be deferred.

Risk: Communication Infrastructure Failure

DERMS control requires reliable communication between each battery system and the central platform. The AEMO trials found that 5–8% of fleet data was missing at any given time in Australia’s well-developed telecommunications environment. In Syria, where telecommunications infrastructure has also been damaged, the risk is substantially higher. Mitigation includes dual-SIM (two-carrier) connectivity for each gateway device, the autonomous Triple-Input logic operating as the primary control mode with central DERMS dispatch as an overlay rather than a dependency, and edge computing at the feeder transformer level to enable localised coordination even when the central platform is unreachable.

Risk: Thermal Degradation of Battery Assets

Syria experiences extreme summer temperatures exceeding 45°C in eastern regions. LiFePO4 chemistry is more thermally robust than NMC alternatives, but sustained high temperatures accelerate calendar ageing. The financial model’s assumption of a 10–20 year asset life depends on adequate thermal management. Mitigation requires passive thermal design standards (ventilated enclosures, shaded positioning, reflective coatings), active cooling for commercial-scale critical node installations, and conservative financial modelling using a 10-year asset life.

3.3 Financial Risks

Risk: Currency Volatility and Revenue Erosion

The Syrian pound has lost approximately 90% of its value since 2011. EaaS subscription revenues will be denominated in local currency, while battery procurement costs are denominated in US dollars or euros. Mitigation strategies include denominational flexibility (subscription fees indexed to a hard currency basket), MDB-provided currency risk facilities, and front-loading procurement during periods of relative stabilisation.

Risk: Slow Financial System Reconnection

Even with sanctions formally lifted, Syria’s banking system reconnection is proceeding slowly. The financing strategy must therefore be sequenced: Phase 1 entirely funded by MDB concessional capital, with commercial bank participation introduced only in Phase 3 once banking channels are normalised.

4. Implementation Roadmap

Phase 0: Institutional Foundation (Months 0–6)

- Establish the Syria Distributed Energy Company (SDEC) as an SPV under the Ministry of Energy.

- Conduct an international tender for the technical and operational partner.

- Secure MDB financing commitment (target: US$50 million IDA/IFC concessional facility).

- Develop the regulatory framework for licensed distributed energy service providers under SEEP Component 3.

- Commission distribution grid assessments in Priority Corridors 1 and 2.

- Design and procure the DERMS platform, specifying edge computing architecture and dual-SIM M2M communication.

Phase 1: Critical Nodes Pilot (Months 6–18)

- Deploy 200–500 systems to critical nodes (health clinics, water pumps, community centres) in the Damascus–Homs corridor.

- Zero end-user cost; funded entirely by MDB grant.

- Focus on demonstrating technical reliability and building public trust.

- Launch the BYOD integration programme, targeting 500–1,000 existing solar-plus-storage systems for DERMS enrolment.

- KPIs: system uptime exceeding 95%; DERMS communication reliability exceeding 92%; measurable reduction in local transformer overloads.

Phase 2: Residential Scale-Up (Months 18–36)

- Expand to 5,000–10,000 household subscriptions across Priority Corridors 1 and 2.

- Introduce the monthly availability fee and grid service credit billing model.

- Establish the Distributed Capacity Procurement (DCP) regulatory framework, enabling PETDE to procure capacity from the SDEC’s aggregated fleet.

- Scale the BYOD programme to 3,000–5,000 integrated systems.

- Target aggregated fleet capacity of 50–75 MW (new installations plus BYOD).

Phase 3: Commercialisation and Regional Integration (Years 3–5)

- Transition financing from concessional MDB terms to commercial bank participation.

- Expand into the Aleppo–Hama corridor as distribution grid rehabilitation progresses.

- Integrate the SDEC’s VPP into the regional electricity interconnection (Jordan–Syria–Turkey) for cross-border frequency regulation.

- Evaluate expansion into northeast Syria contingent on political settlement.

- Target aggregated fleet capacity of 150–250 MW.

5. Financial Architecture

5.1 Capital Structure

The programme’s total capital requirement across the five-year roadmap is estimated at US$180–280 million, depending on the pace of scale-up and the proportion of BYOD versus new installations. The BYOD track is significantly less capital-intensive, requiring only gateway devices and DERMS integration rather than full battery system procurement.

Source | Phase 1 | Phase 2 | Phase 3 | Instrument |

IDA/IFC Concessional | US$30–40M | US$40–60M | — | Grant + concessional loan |

Bilateral (EU/GCC) | US$5–10M | US$15–25M | US$10–20M | Tied technical assistance |

Commercial Debt | — | — | US$40–80M | Project finance (MIGA-backed) |

Subscriber Revenue | Negligible | US$3–6M/yr | US$10–20M/yr | Availability fees + grid credits |

5.2 De-Risking Instruments

- Sovereign Risk Guarantees: MIGA or similar guarantees protecting against government default, expropriation, and currency transfer restrictions, reducing the cost of capital by an estimated 20–30%.

- Energy Savings Insurance: A performance guarantee instrument modelled on the IDB’s Energy Savings Insurance programme, guaranteeing a minimum level of energy savings to build lender confidence.

- First-Loss Facility: An MDB-funded tranche absorbing the first 15–20% of portfolio losses, enabling commercial lenders to participate at reduced risk.

- Political Risk Insurance: Specific coverage for conflict-related asset loss or damage, priced at a premium but essential for the Syrian context.

5.3 Revenue Model Sensitivity

Conservative modelling should assume that grid service revenues are negligible in Phase 1 (as the distribution grid may not support VPP dispatch), begin to materialise in Phase 2 as distribution rehabilitation progresses, and reach full potential only in Phase 3 when the VPP is large enough (150+ MW) to participate meaningfully in regional markets. The availability fee must therefore cover operating costs and debt service even in the absence of grid service revenues during early phases. This reflects the AEMO finding that VPP grid-services revenue alone was insufficient to sustain the financial model at small scale.

6. Cybersecurity Architecture

A network of thousands of internet-connected battery endpoints, each capable of injecting or withdrawing power from the grid, presents a target set that requires a dedicated security architecture. Syria’s energy infrastructure has been a strategic target for over a decade, and the threat environment is qualitatively different from that of developed-market VPP programmes. The framework proposes a defence-in-depth architecture across four layers.

- Device Layer: Each battery inverter and gateway device must implement hardware-enforced SoC floors (the Resilience Reserve) that cannot be overridden by software commands. Firmware updates must be cryptographically signed and verified before installation.

- Communication Layer: All telemetry and control signals must use end-to-end encryption (TLS 1.3 minimum). Dual-SIM M2M connectivity provides redundancy. Communication failures must default to autonomous Triple-Input operation, not to a permissive state.

- Edge Layer: Feeder-level edge computing nodes provide localised coordination, can operate independently if the central platform is unreachable, and reduce the attack surface exposed to the internet.

- Central Platform: The DERMS platform must be hosted in a secure, geographically redundant environment (not on Syrian infrastructure in Phase 1). Access control, audit logging, and anomaly detection must meet ISO 27001 standards.

A dedicated cybersecurity function within the SDEC, staffed by or contracted from the international technical partner, should conduct regular penetration testing and maintain an incident response plan. The cost of this function should be budgeted explicitly as a core operational expense.

7. Political Economy Strategy

7.1 Engaging the Existing Solar Industry

During the conflict, a substantial ecosystem of solar equipment importers, installers, and maintenance providers emerged. Under the Assad regime, a Renewable Energy Support Fund was established with 428 accredited entities across Syrian governorates. While the quality and integrity of these entities varies, they represent a workforce and supply chain that the SDEC should absorb rather than bypass. The SDEC should establish an accreditation programme for existing solar installers, offering certified installers the opportunity to serve as the local installation and first-line maintenance workforce for the EaaS programme. This creates employment, reduces the SDEC’s operational costs, and builds local buy-in, applying the lesson from Lebanon’s Zahle that community-level ownership is essential for sustainability.

7.2 Municipal Integration

In areas where municipalities have functional governance, the SDEC should establish formal cooperation agreements. Municipalities can assist with site identification for critical node installations, serve as community liaison points to build public trust, and benefit from reduced pressure on local infrastructure when household energy reliability improves. This is particularly important in the Homs–Hama corridor where local industrial zones have already demonstrated capacity for renewable energy integration, with 40 MW of solar connected at the Hassia Industrial Zone.

7.3 Transparent Communication Strategy

The Resilience Reserve and the real-time mobile application are technical features, but their primary function is political: they demonstrate that the programme serves the household, not just the grid. The communication strategy should emphasise the household benefit (backup power, reduced generator dependence) first, and the grid benefit (peak shaving, stability) second. In a post-conflict society where state promises carry little credibility, demonstrated performance is the only effective communication tool. GMP’s experience in Vermont, where the programme’s popularity was driven by tangible outage protection rather than abstract grid benefits, confirms this principle.

7.4 Climate Resilience Integration

Syria’s reconstruction must account for rising temperatures, declining precipitation, and increasing frequency of extreme heat events. The ODI is currently preparing a climate risk assessment of Syria’s electricity system, due for publication in April 2026. Battery storage performance degrades in extreme heat; while LiFePO4 is more thermally stable than NMC alternatives, operating temperatures in Syrian summers routinely exceed 40°C. All installations must incorporate passive thermal management standards (ventilated enclosures, shaded positioning, reflective coatings), and the programme’s monitoring system should track cell temperature as a leading indicator of asset degradation.

8. Conclusion

International evidence from Vermont, Australia, Lebanon, and South Australia demonstrates that utility-led distributed energy storage is a proven model for transforming fragmented energy landscapes into coordinated, resilient systems. The technology works. The financial models are maturing. The household-level value proposition is compelling. But the evidence also shows, with particular clarity from Lebanon, that delay is costly: once fragmented energy provision consolidates into an entrenched parallel economy with political protection, reform becomes exponentially harder.

Syria faces precisely this risk. The grassroots adoption of 1.4 GW of standalone solar-plus-storage during the conflict was a rational survival response, but if this base is not integrated into a coordinated system, Syria risks replicating Lebanon’s outcome: a dual-tier energy economy where the wealthy enjoy private solar independence and the poor remain trapped in unreliable grid dependency or expensive generator subscriptions.

This proposal addresses this challenge through the establishment of a dedicated SPV (the SDEC) to insulate the programme from PETDE’s institutional constraints; a geographic targeting strategy (“Corridors of Confidence”) that concentrates deployment in areas of stability; a two-track approach (new utility-owned systems plus BYOD integration) that engages the existing solar asset base; a sequenced financing architecture that bridges the gap between sanctions relief and financial system normalisation; a defence-in-depth cybersecurity architecture; and a political economy strategy that incorporates existing industry actors rather than displacing them.

The window for action is narrow. Syria’s energy crisis is the most immediate threat to the political legitimacy of the transitional government and to the economic recovery upon which refugee return depends. The large-scale centralised generation projects currently under negotiation will take three to five years to deliver meaningful increases in supply. In the interim, a well-designed distributed EaaS programme can provide visible, household-level improvement in energy reliability while building the institutional and technical infrastructure for a modern, digitally orchestrated energy system. The choice is not between centralised and distributed investment; it is whether Syria seizes the opportunity to build both simultaneously.

References

Karam Shaar Advisory Ltd. (2025). ‘Obstacles and Opportunities for Syria’s Electricity Sector.’ Syria in Figures series. Published 11 October 2025. Available at: https://karamshaar.com/syria-in-figures/obstacles-and-opportunities-for-syrias-electricity-sector/

Karam Shaar Advisory Ltd. (2025). ‘Electricity Situation in Syria 2025: Paths to Recovery.’ Syria in Figures series. Published 13 October 2025. Available at: https://karamshaar.com/syria-in-figures/powering-the-recovery-the-electricity-sector-at-a-crossroads/

Levant24 (2025). ‘Rebuilding Electrical Infrastructure in Liberated Syria.’ Published 2 January 2025. Available at: https://levant24.com/news/national/2025/01/rebuilding-electrical-infrastructure-in-liberated-syria/

Levant24 (2026). ‘Strategic Electricity Projects Strengthen Syria’s National Grid.’ Published 9 January 2026. Available at: https://levant24.com/news/2026/01/strategic-electricity-projects-strengthen-syrias-national-grid/

Wikipedia (2026). ‘Electricity in Syria.’ Last updated 23 February 2026. [Used for historical generation data, pre-conflict capacity figures, and Law 32 of 2010 regulatory context.] Available at: https://en.wikipedia.org/wiki/Electricity_in_Syria

The National (2025). ‘Syria’s electricity situation improving with foreign support, report finds.’ Published 2 September 2025. Available at: https://www.thenationalnews.com/news/mena/2025/09/02/syrias-electricity-situation-improving-with-foreign-support-report-finds/

World Bank (2025). ‘Syria: World Bank US$146 Million Grant to Improve Electricity Supply and Support Sector Development.’ Press release, 25 June 2025. Available at: https://www.worldbank.org/en/news/press-release/2025/06/25/syria-world-bank-us-146-million-grant-to-improve-electricity-supply-and-support-sector-development

World Bank (2025). ‘The World Bank Syria Electricity Emergency Project (P511407).’ Project Appraisal Document, 6 June 2025. Available at: https://documents1.worldbank.org/curated/en/099060625055567160/pdf/P511407-afa010d5-6fc0-4c0d-859d-79b01a31c3f5.pdf

Syrian Ministry of Energy / PETDE (2025). ‘Environmental and Social Commitment Plan (ESCP)’ for SEEP Project. Published 26 May 2025. Available at: http://moe.gov.sy/news/details/417

World Bank (2025). ‘Syria Electricity Emergency Project (SEEP) – Early Market Engagement Workshop.’ Event page, 23 July 2025. Available at: https://www.worldbank.org/en/events/2025/07/23/syria-electricity-emergency-project-seep-early-market-engagement-workshop

Economy Middle East (2025). ‘World Bank approves $146 million grant to restore electricity in Syria.’ Published 25 June 2025. Available at: https://economymiddleeast.com/news/world-bank-approves-146-million-grant-to-restore-electricity-in-syria/

Modern Diplomacy (2026). ‘Syria’s energy comeback amid challenges.’ Published 4 February 2026. Available at: https://moderndiplomacy.eu/2026/02/04/syrias-energy-comeback-amid-challenges/

The Washington Institute (2025). ‘Maintaining Momentum in Syria’s Energy Sector.’ Policy Analysis. Available at: https://www.washingtoninstitute.org/policy-analysis/maintaining-momentum-syrias-energy-sector

Al Jazeera (2026). ‘Power lines and power struggles: Unpacking Syria’s push towards unification.’ Published 19 January 2026. Available at: https://www.aljazeera.com/news/2026/1/19/power-lines-and-power-struggles-unpacking-syria-push-towards-unification

TaiyangNews (2025). ‘Qatar-Led Partnership To Build 1 GW Solar Facility In Syria.’ Published 30 May 2025. Available at: https://taiyangnews.info/markets/syria-plans-1-gw-solar-power-plant

EU Institute for Security Studies (2025). ‘Energising Syria’s future.’ Commentary, 19 August 2025. Available at: https://www.iss.europa.eu/publications/commentary/energising-syrias-future

TaiyangNews (2025). ‘Syria Announces 100 MW Solar PV Power Project.’ Published 1 September 2025. Available at: https://taiyangnews.info/markets/syria-plans-100-mw-solar-energy-project

PV Tech (2025). ‘Syria signs deal with STE to build 100MW solar PV plant.’ Published 1 September 2025. [Includes IRENA data: 60 MW installed solar capacity as of 2023.] Available at: https://www.pv-tech.org/syria-signs-deal-with-ste-to-build-100mw-solar-pv-plant/

Syria Capital Partners (2026). ‘Are There Planned Solar Farm Projects in Syria?’ Published 9 February 2026. Available at: https://syriacapitalpartners.com/blog/are-there-planned-solar-farm-projects-in-syria/

Syria Capital Partners (2026). ‘Solar Part of Rebuilding Syria’s Infrastructure.’ Published 6 March 2026. Available at: https://syriacapitalpartners.com/blog/solar-part-of-rebuilding-syrias-infrastructure/

PVKnowhow (2026). ‘Solar Panels Syria 2025: 5 Essential Insights for Progress.’ Published April 2026. [Source for 1.4 GW standalone solar+storage estimate and ACWA Power 2.5 GW agreement.] Available at: https://www.pvknowhow.com/news/solar-panels-syria-2025-no-press-releases/

Alnasser, Y. et al. (2025). ‘Renewable resilience in conflict: lessons learned from Syria’s solar-powered electric health vehicles.’ Frontiers in Public Health. [PMC open access.] Available at: https://pmc.ncbi.nlm.nih.gov/articles/PMC12000051/

Al Jumhuriya (2025). ‘Solar Energy in Syria.’ Published 14 March 2025. [Investigative report on the Renewable Energy Support Fund and 428 accredited entities.] Available at: https://aljumhuriya.net/en/2025/03/14/solar-energy-in-syria/

ODI (2026). ‘Climate and financial risks to Syria’s electricity system.’ Briefing paper announcement, 6 March 2026. [Full paper forthcoming April 2026.] Available at: https://odi.org/en/publications/climate-and-financial-risks-to-syrias-electricity-system/