The New Frontier of Real Estate Integrity

Decarbonisation and the Residual Emission Challenge

In the rigorous pursuit of net zero, the commercial real estate (CRE) sector has reached a defining threshold. While direct mitigation efforts, such as deep energy retrofits and the electrification of heating systems, remain the primary focus of credible climate strategies, an inescapable reality persists: the challenge of residual emissions. These are the emissions that remain within Scopes 1, 2, and 3 after all feasible technical and operational measures have been exhausted. For the discerning real estate leader, the procurement of high-integrity carbon credits is no longer a peripheral philanthropic exercise but a strategic necessity for addressing these recalcitrant offsets. This is particularly acute in the context of embodied carbon (Scope 3), where the emissions tied to construction materials and the supply chain often remain stubbornly high even as operational efficiency (Scopes 1 and 2) improves.

The demand for carbon credits within the CRE sector is being propelled by a confluence of powerful drivers. Institutional investors increasingly demand concrete evidence of transition planning, while tenants seek net zero-aligned spaces to satisfy their own corporate sustainability mandates. Simultaneously, the UK regulatory environment has become significantly more demanding. Frameworks such as Streamlined Energy and Carbon Reporting (SECR), the Task Force on Climate-related Financial Disclosures (TCFD), and the anticipated Sustainability Disclosure Requirements (SDR) are forcing a new level of transparency regarding climate strategies and the role of offsetting. Failure to navigate this landscape carries profound risks, not merely in terms of reputational damage but through the potential for “stranded assets” that no longer meet investor or regulatory benchmarks.

Historically, the voluntary carbon market (VCM) has been an opaque and fragmented arena, often lacking the standardisation required for institutional-grade decision-making. In response to this, the Better Buildings Partnership (BBP) has stepped forward to provide much-needed structure. By synthesising emerging best practices from global integrity bodies, the BBP offers a framework that allows real estate firms to navigate the market with consistency and confidence (BBP, 2025). This guidance is vital as the industry moves away from ad hoc, end-of-year ‘top-up’ purchases toward more sophisticated, long-term procurement strategies. To master this new frontier, one must first deconstruct the fundamental mechanics of the VCM and the instruments it provides.

Deconstructing the Voluntary Carbon Market Actors and Instruments

The VCM is a complex ecosystem where understanding market structure serves as a firm’s first line of defence against significant reputational and operational risks. Without a clear grasp of market actors and instruments, a buyer risks engaging in transactions that may later be branded as ‘greenwashing’ by stakeholders or regulators. Understanding the chain of custody for a carbon credit is paramount for ensuring that a claim of neutrality is legally and scientifically robust.

At the heart of the market are the Project Developers, the entities that design and implement projects (such as reforestation or the distribution of clean cookstoves) to generate credits. These projects are governed by Crediting Programmes and Registries, such as Verra (the Verified Carbon Standard) or the Gold Standard. These organisations define the methodologies for what constitutes a valid credit and maintain registries to ensure that each unit is unique and tracked. Brokers and Retailers act as the essential intermediaries, curating portfolios and providing the advisory services required for a buyer to select appropriate projects. Finally, the End Buyer (typically the property company or fund manager) purchases these credits to compensate for residual emissions.

The instruments themselves vary significantly in their climate impact and risk profile. Understanding the distinction between avoidance and removal, and the timing of issuance, is essential for long-term net zero alignment.

Instrument Category | Type | Strategic Implication for Real Estate |

Climate Mechanism | Avoidance | Prevents emissions that would have occurred (e.g. forest conservation). Often lower cost but faces increasing scrutiny regarding long-term additionality claims. |

Removal | Extracts carbon from the atmosphere (e.g. biochar, afforestation). Viewed as the gold standard for long-term net zero alignment. | |

Timing of Issuance | Ex-post | Credits issued after verification of the climate benefit. Lower risk, as the impact is already achieved. Suitable for spot purchases. |

Ex-ante | Credits issued based on projected future removals (e.g. Pending Issuance Units). Carries delivery risk but supports early-stage projects. | |

Durability | Durable | Carbon is stored for 40+ years per ICVCM thresholds, though technical methods like mineralisation offer storage for centuries. |

Reversible | Risk of carbon re-release (e.g. forestry fire). Requires robust buffer pools and ongoing monitoring. |

To elevate market integrity, several overarching bodies have established benchmarks that buyers should seek. The Integrity Council for the Voluntary Carbon Market (ICVCM) has developed the Core Carbon Principles (CCPs), while the International Carbon Reduction and Offset Alliance (ICROA) provides an essential code of best practice for market participants (ICROA, 2025). Adherence to these standards provides a layer of assurance that the credits purchased represent genuine, measurable climate benefits. Understanding these market fundamentals is the prerequisite for implementing a structured procurement process that can withstand the rigours of external audit.

The Architecture of Procurement: A Five-Stage Framework

For the modern real estate firm, the era of ad hoc ‘spot’ purchases made in the final weeks of a reporting cycle is ending. Managing the complexities of carbon integrity requires moving toward a structured, repeatable procurement process that can withstand external scrutiny. The BBP outlines a five-stage framework designed to integrate carbon credit procurement into the broader asset and portfolio management lifecycle.

Stage 1: Identification of Requirements

The process begins by defining the quantity and timing of emissions that require compensation. This involves aligning credit requirements with specific organisational goals. For instance, a developer may seek one-off spot purchases to offset the embodied carbon of a single asset for BREEAM certification, whereas a fund manager might require a multi-year forecast to address residual operational emissions across a diversified portfolio. Failure at this stage often leads to “under-procurement,” resulting in a late-cycle scramble for low-quality credits that may not meet the firm’s stated ESG criteria.

Stage 2: Development of a Procurement Specification

Success in procurement is often determined by the quality of the initial specification. Firms must translate their high-level climate principles into a ‘procurement-ready’ document. According to the BBP, this document should be built upon seven core components: Standards and Certification Requirements, Assessment Criteria, Procurement Format and Terms, Portfolio Goals and Mix, Eligibility Constraints, Industry Alignment, and Additional Preferences (BBP, 2025). A robust specification acts as a safeguard, mitigating the risk of future litigation or accusations of greenwashing by ensuring that all prospective suppliers are measured against the same quality benchmarks.

Stage 3: Approach and Evaluation of Suppliers

In this stage, the firm engages the market through Requests for Information (RFI) or Requests for Proposals (RFP). This is where the theoretical requirements of Stage 2 are tested against market reality. The focus here is on identifying credible partners who can demonstrate a track record of transparency and reliability. From a commercial standpoint, failing to vet the intermediary properly can lead to “intermediary risk,” where the broker fails to provide the necessary retirement certificates, leaving the firm unable to verify its climate claims during a financial audit.

Stage 4: Selection and Negotiation

Once the evaluation is complete, the firm moves to finalise contract terms. This requires negotiating delivery timelines, verification milestones, and remedies for non-performance. For long-term agreements, this is the stage where pricing structures (e.g. indexed versus fixed) and reporting protocols are codified. A critical commercial consequence of failure here is the lack of price indexing or non-performance remedies, which could lead to a multi-million-pound balance sheet liability if the carbon credits are subsequently disqualified by integrity bodies or if the project fails to deliver the expected volume.

Stage 5: Procurement and Onboarding

The final stage involves formalising the purchase and ensuring the provider is integrated into the firm’s reporting infrastructure. This ensures that credits are properly retired on the relevant registry and that documentation is archived for future audits. Without proper onboarding, the data gap between the procurement team and the ESG reporting team can result in public disclosures that are inaccurate or outdated, inviting regulatory intervention.

The Ten Pillars of Carbon Integrity: The Due Diligence Framework

Project quality in the carbon market is not a binary state; it exists on a spectrum of risk. To help buyers navigate this, the BBP has identified ten key principles of carbon integrity, largely derived from the ICVCM benchmarks. A ‘model answer’ for a CRE buyer involves ensuring that projects meet high-level standards across each pillar.

- Effective Governance: The carbon-crediting programme must operate with transparency and accountability, typically evidenced by independent board oversight and robust anti-corruption policies.

- Tracking: Credits must be uniquely identified on a publicly accessible registry to ensure they are not sold multiple times.

- Transparency: All project information, including ownership and methodology, must be publicly available for scrutiny.

- Independent Verification: Projects must be validated and verified by qualified third-party assessors.

- Additionality: The emissions reductions must not have occurred in the absence of the carbon credit revenue. An essential executive insight here is the revenue threshold: if carbon credit revenue accounts for 5% or less of total project revenue, additionality should be subject to intense scrutiny to ensure the project is not simply “business as usual.”

- Permanence: The climate benefit must be lasting. For removal projects, there must be a plan to mitigate ‘reversal’ (e.g. fire or disease) through buffer pools or insurance.

- Robust Quantification: Emissions benefits must be calculated using conservative, scientifically validated methods.

- No Double Counting: Procedures must be in place to ensure credits are only counted once toward a mitigation target.

- Sustainable Development Benefits: Projects should provide co-benefits, such as biodiversity protection or community employment, backed by quantified evidence.

- Contribution to Net Zero: The project must not lock in technologies or practices that are incompatible with reaching net zero by mid-century.

Additionality and Permanence serve as the dual cornerstones. If a project fails to prove it is additional, it represents no real change to the atmosphere; if it fails on permanence, its climate benefit is merely temporary. Furthermore, for CRE developers, the “Contribution to Net Zero” pillar must account for the emissions generated during the project’s own implementation, including those from Non-Road Mobile Machinery (NRMM). If construction machinery used in a reforestation project is not accounted for, the net climate benefit is diminished (BBP, 2025).

Operationalising Diligence: The RFI and RFP Mechanisms

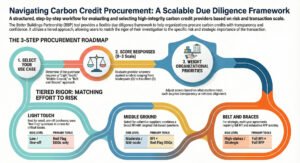

To ensure procurement efficiency, a tiered approach to due diligence is recommended. This allows firms to screen suppliers broadly before committing resources to a deep-dive project analysis. Diligence is not a monolith; it is a tactical choice calibrated against the scale of the commitment.

The Request for Information (RFI)

The RFI is a strategic tool for broad supplier screening. It is used to evaluate the credibility, track record, and fee transparency of a broker or retailer. A model RFI response should provide clear details on the provider’s history, their internal due diligence processes, and their ability to provide multi-year capacity. For a senior manager, the RFI serves to identify whether the intermediary is a reliable partner before specific projects are even discussed.

The Request for Proposal (RFP)

The RFP is reserved for deep-dive project scrutiny. It demands technical documentation, such as Project Design Documents (PDDs) and Monitoring Reports. At this stage, the firm evaluates the specific methodology of a project, its baseline quantification, and its social impacts. This level of detail is necessary to justify the expenditure to investment committees and auditors.

The ‘Red Flag’ System

A critical component of this diligence is the ‘Red Flag’ system. Senior managers must treat certain issues as non-negotiable failure points. These include:

- A lack of listing on a recognised public registry (e.g. Verra, Gold Standard).

- The absence of third-party independent verification.

- Inability to provide a clear fee breakdown between the intermediary and the project developer.

- Failure to confirm that the project is not legally mandated or already a requirement of local planning policy.

Documentation that a senior manager should demand includes the PDD, which outlines the project’s intent and interventions; Technical Specifications, which provide the scientific foundation; and Audit Reports, which validate the claims made by the developer. This documentation forms the audit trail that protects the firm from greenwashing accusations.

Use Cases and Weighted Scoring

A sophisticated procurement strategy recognises the necessity of a ‘proportionate’ approach to risk management. Not every purchase requires the same level of scrutiny, and resources should be allocated where the potential for reputational or financial loss is greatest.

Use Case | When to Use | What It Looks Like (Sequence) |

Light Touch | Low-value, one-off transactions (e.g. year-end top-up). | Only Red Flag DDQs used to screen for critical issues. No RFI or Full DDQ. |

Middle Ground | Moderate-risk or medium-scale purchases with unfamiliar suppliers. | Stage 1: RFI to understand supplier credibility. Stage 2: Red Flag DDQs. (Full DDQ only if clarity is needed). |

Belt and Braces | Strategic, high-stakes transactions (e.g. multi-year offtakes). | Stage 1: RFI. Stage 2: Full deployment of Red Flag and Full DDQs for exhaustive review. |

Scoring and Weighting

To compare providers objectively, firms should employ a scoring rubric (typically 0–3). However, the importance of different themes should be adjusted based on the procurement context. For a ‘Short-term Spot Purchase’, the weighting may be higher for Fee Transparency and Carbon Verification Methods to ensure immediate delivery and value. Conversely, for a ‘Strategic Multi-year Offtake’, the weighting should shift heavily toward Permanence, Additionality, and Multi-year Capacity Assurance. This ensures that the evaluation is aligned with the firm’s long-term sustainability strategy rather than just short-term compliance. Adjusting weightings allows an organisation to reflect its specific risk appetite; for instance, a firm with high public visibility may weight Sustainable Development Benefits more heavily to bolster its social impact narrative.

Risk Mitigation and Market Evolution

The voluntary carbon market remains volatile, characterised by shifting standards and emerging regulations. A dynamic strategy is required to protect the long-term value of a real estate portfolio’s climate claims. As the market matures, the cost of “integrity” is likely to rise, making early strategic procurement a financial hedge against future price spikes.

Sophisticated Risk Mitigation

Sophisticated buyers are increasingly using tools to hedge against the risk of project failure or reputational damage. Diversification is a primary strategy: sourcing credits across different project types (e.g. peatland restoration and biochar) and diverse geographies to reduce over-reliance on a single regulatory or environmental outcome. Furthermore, Offset Insurance and the utilisation of Buffer Pools (reserves of credits set aside by registries to cover reversals) are becoming standard requirements for institutional-grade projects. A firm that ignores these safeguards risks a “carbon default” should their chosen project suffer a catastrophic reversal, such as a wildfire, without a contractual right to replacement credits.

The Global Context: Article 6 and Corresponding Adjustments

The evolution of the market is also being shaped by Article 6 of the Paris Agreement. For CRE firms, the future of high-integrity claims may depend on ‘Corresponding Adjustments’. These are accounting mechanisms that ensure emissions reductions are not double-counted by both the project host country and the private buyer. As international carbon accounting matures, credits that include these adjustments are likely to command a premium and be viewed as the only viable option for making “net zero” claims that withstand international scrutiny.

The Shift to Durable Removals

There is a clear market trajectory from ‘Avoidance’ credits (preventing emissions) to ‘Durable Removals’ (extracting carbon). Aligned with the Oxford Principles, the strategic goal for most CRE net zero pathways is to transition toward 100% removals with high durability (Oxford Principles, 2024). This transition must be managed carefully, as the scarcity of durable removal credits like Direct Air Capture (DAC) or mineralisation (which ensures carbon storage for centuries) requires long-term offtake commitments to secure supply.

The role of transparency in building long-term sector resilience cannot be overstated. A commitment to rigorous due diligence, clear disclosure, and a proactive approach to risk management is the only path to a defensible climate strategy. By adopting the structured frameworks provided by the BBP, real estate market participants can ensure that their carbon credit procurement is not merely an expense, but a robust contribution to a net zero future (UKGBC, 2024).

References

- Better Buildings Partnership (2025). Carbon Credit Procurement Guide. London: Better Buildings Partnership. https://www.betterbuildingspartnership.co.uk/carbon-credit-procurement-guide

- Carbon Credit Quality Initiative (2022). Methodology for Assessing the Quality of Carbon Credits. https://www.oeko.de/en/publications/methodology-for-assessing-the-quality-of-carbon-credits/

- ICVCM (2024). Core Carbon Principles. Integrity Council for the Voluntary Carbon Market. https://icvcm.org/core-carbon-principles/

- International Carbon Reduction and Offset Alliance (2025). ICROA Code of Best Practice. https://icroa.org/approval/icroa-code-of-best-practice/

- Oxford Principles (2024). The Oxford Principles for Net Zero Aligned Carbon Offsetting. Oxford: University of Oxford. https://www.smithschool.ox.ac.uk/research/oxford-offsetting-principles

- Science Based Targets initiative (2024). Beyond Value Chain Mitigation (BVCM) Guidance. https://sciencebasedtargets.org/beyond-value-chain-mitigation

- Stockholm Environment Institute (2019). Securing Climate Benefit: A Guide to Using Carbon Credits. https://www.sei.org/publications/guide-to-using-carbon-offsets/

- UKGBC (2024). Carbon Offsetting and Pricing Report. London: UK Green Building Council. https://ukgbc.org/our-work/topics/advancing-net-zero/carbon-offsetting-and-pricing/

- Voluntary Carbon Markets Integrity Initiative (2023). Claims Code of Practice. VCMI. https://vcmintegrity.org/vcmi-claims-code-of-practice/